Washington announces new stockpile initiative, as data reveals the extent of the turmoil in critical mineral imports

What you’ll learn in this article:

- The havoc caused by tariffs and export controls in critical minerals markets.

- The erosion of America’s dependency on China for critical minerals.

- The lessons all companies can learn from the government’s Project Vault strategy, regardless of their sector.

🎯 Best for: Supply chain directors, policy analysts, business strategists, and executives in mining, metals and advanced manufacturing.

In 2025, U.S. import volumes of key critical minerals swung dramatically within months, some collapsing, others spiking, as tariffs and export controls reshaped global supply chains in real time.

Now Washington is responding with a $12 billion bet: Project Vault. The move is an attempt to circumvent recent export restrictions enacted by China, the world’s leading producer and processor of critical minerals.

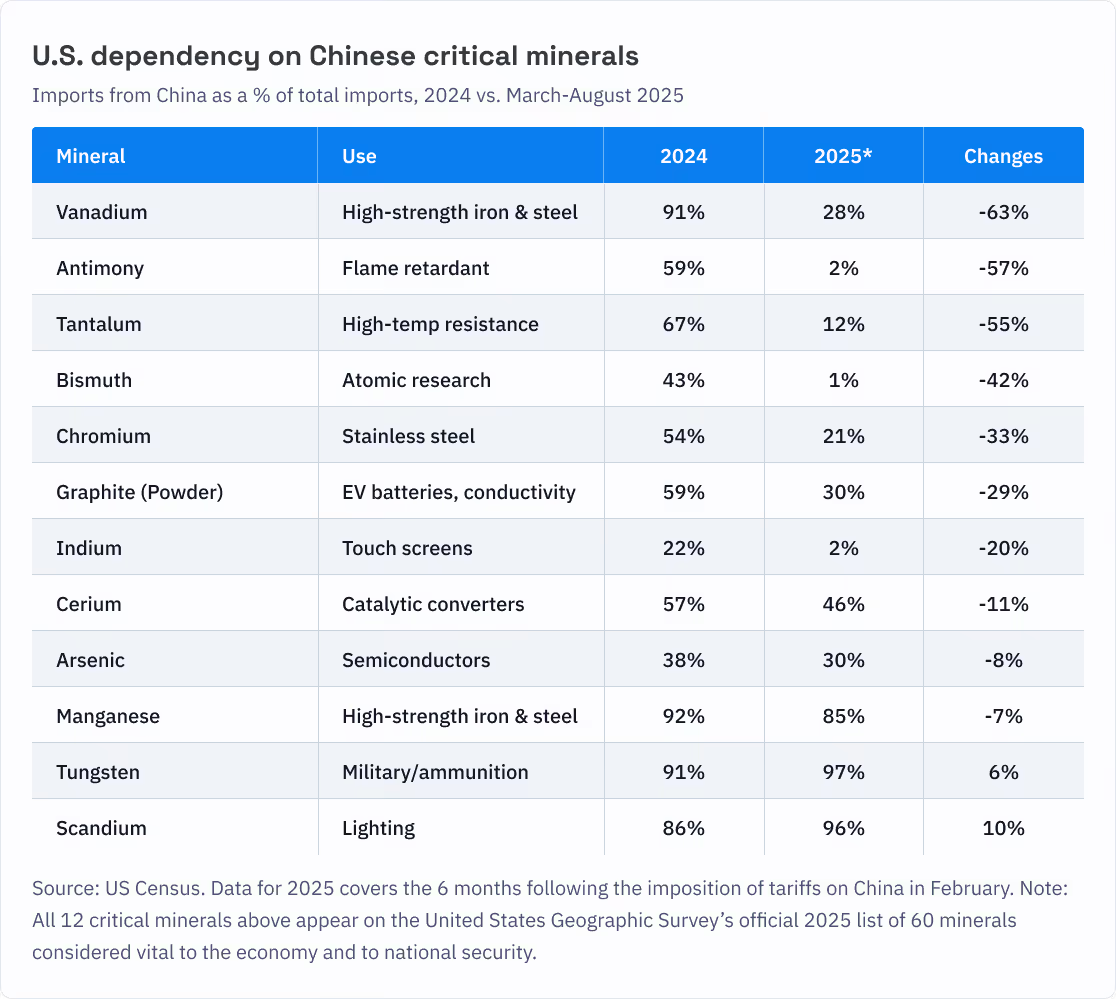

U.S. Census data analyzed by ImportGenius shows that critical mineral imports fluctuated wildly in 2025, as American industry sought alternative sources for a number of key inputs. “American industry has been looking to diversify its critical mineral supply chains for years, but the events of 2025 appear to have forced everyone’s hand,” says ImportGenius CEO Michael Kanko. “The combination of high U.S. tariffs and export controls from China produced dramatic changes in import patterns.”

American dependency on China appears to be waning

Critical minerals have been a hot-button issue in the relationship between America and China for years. But the issue heated up significantly in early 2025 when the United States first imposed new tariffs on Chinese imports. In response to those tariffs, and to U.S. export controls on computer chips, China retaliated by restricting the export of critical minerals and rare earths. “Critical minerals have become China’s most effective trade lever,” says Kanko.

The results have been mixed. ImportGenius compared U.S. critical mineral imports coming from China in 2024 with those coming between March and August 2025, when tariffs on China reached peak levels. The data shows that China’s dominance for many of those imports is eroding.

The data is striking, with China’s share of total imports falling precipitously in a number of key categories, and rising in others. Among the highlights:

- Graphite (-29%): China is the world’s largest graphite producer and refiner, creating materials that are used in most EV batteries. But the proportion of graphite powder imports coming from China fell in response to tariffs and export controls as American automakers scaled back investments in electric vehicle production.

- Indium (-20%): An essential component of touch screens and LCD displays, Indium became subject to export controls last February, when the U.S. first imposed a 10% tariff on Chinese goods.

- Manganese (-7%): The U.S. appears to be slowly weaning off its dependency on China for this key element in the production of high-strength steel, from heavy-duty machinery to gun barrels.

- Tungsten (+6%): The U.S. increased its reliance on China in 2025 for tungsten. But China’s export controls resulted in a significant reduction in total imports of the substance, which is used in multiple military applications.

Impacts ripple throughout the economy

Critical minerals are not just an issue for the mining sector: their availability impacts multiple industries and has implications for national security. Critical minerals are essential for many advanced manufacturing industries, including automotive, defense, aerospace, and computing — industries that employ tens of thousands of workers. Critical minerals price increases, shipment delays and shortages can potentially lead to assembly line slowdowns and closures. Further down the line, they can also lead to inventory shortages, including for munitions and other defense matériel.

“Critical minerals are a choke point for the rest of the economy because they are essential inputs for so many industries,” says Kanko. “Any business that supports these sectors, even if they don’t directly purchase or deal in critical minerals, needs to monitor this issue.”

The potential of Project Vault: the lesson for business

Overall, the data points to a significant reduction in dependency upon China as a source of critical minerals, albeit with significant fluctuations in import volumes and suppliers.

“There’s a tremendous amount of volatility in critical minerals markets right now,” says Kanko. “The Project Vault stockpile, if successful, would hinder China’s ability to control global access and restore a measure of market predictability.”

Project Vault is a long-term initiative that will take years to come to fruition. In the meantime, the Trump administration has signed agreements to explore critical minerals opportunities with (among others) Canada, Mexico, and the G7 group of nations. It has also taken an equity stake in a number of private-sector mining companies.

“The United States government is doing what all companies should be doing, no matter what sector they operate in,” says Kanko. “They’re protecting their interests from future market disruptions and policy changes. And they’re doing it by stockpiling, investing in alternatives, and diversifying their supply chain to other parts of the world.”

[CT1]

Stockpile, diversify, or both?

Stockpile, diversify, or both?

More blogs & reports